Today I am writing about six of the best blue-chip stocks under $20 that are worth buying now. These stocks also have the distinction of having very low price-to-earnings (P/E) multiples and producing enough earnings to cover dividend payments to shareholders.

It’s actually harder than you think to find these stocks. Typically if a company has good earnings and pays a dividend well-covered by earnings the price will be significantly higher than $20.

Moreover, these stocks are all very cheap. Their average P/E multiple is just 4.5x on a median basis.

The average stock on this list has an 8.43% dividend yield, but that is highly skewed by the 18.6% yield of one stock. As a result, the median yield is 7.42%. These stocks have also performed well so far this year. The average YTD performance is down just 8%.

One of the benefits of these stocks is that it is easier to create covered call income with stocks below $20 per share. That is because every option contract that you sell out-of-the-money requires the purchase of 100 shares to “cover” those shares. I will provide several examples of these covered call plays.

Let’s dive in and look at the six best blue-chip stocks under $20.

| CPG | Crescent Point Group | $6.65 |

| GRIN | Grindrod Shipping Holdings | $15.92 |

| GNK | Genco Shipping and Trading Ltd | $17.02 |

| CVE | Cenovus Energy | $16.30 |

| F | Ford | $11.88 |

| CGBD | Carlyle Secured Lending | $12.73 |

Crescent Point Group (CPG)

Market Cap: $3.76 billion

Crescent Point Group (NYSE:CPG), the first on this list of the best blue-chip stocks under $20, is an oil and gas producer in Western Canada and in the U.S. (North Dakota and Montana). The company is now very profitable and earnings per share (EPS) this year are forecast to hit $2.86. This puts the stock on a forward P/E multiple of 2.3x.

However, next year, analysts forecast that with projected lower oil and gas prices, its earnings will fall. They now see EPS declining 40% to $1.72.

However, even if that happens, the resulting higher P/E multiple is just 3.9x. That is still incredibly inexpensive. So that might now mean the stock will take a hit and in fact, it could be relatively stable.

Moreover, the stock also pays an annual dividend of 24.52 cents per share, giving the investor an annual yield of 3.7%. In fact, the company recently just raised its dividend.

All this makes CPG stock, at $6.65 per share at Friday’s close, a reasonably good candidate for an out-of-the-money play. Here’s why. For $2,000, we can actually buy 300 shares (i.e., $1,995) and then sell three out-of-the-money covered call options. Let’s look at that.

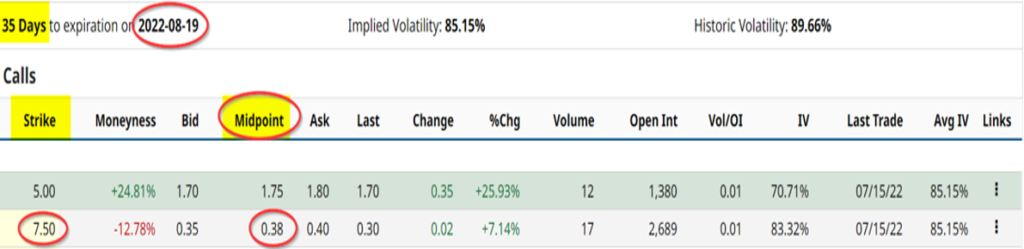

The Barchart option chain below shows that the Aug. 19 call options offer the $7.50 strike price calls at 38 cents at the midpoint.

Here is what that means. We can sell three covered call options at the $7.50 strike price and immediately receive $38 per call contract, or $114 total, less any commissions. That is a very good income, since we only paid $1,995 for the underlying stock, effectively a monthly return of 5.714%. These monthly options can potentially be repeated, so the theoretical annual return is 68.57%.

This assumes the stock does not immediately rise to the $7.50 strike price by Aug. 19 or earlier. But even if it does, the investor collects the capital gain, which will be 12.78% (i.e., $7.50/6.65 cost), or $2,250-$1,995 = $255.

So the total return, even without the dividends will be 18.49% (12.78% + 5.71%). In other words, the investor collects $255, plus the $114 from the covered calls, or $369. This is a return of 18.49% on the investor’s intial cost of $1,995.

This large profit is possible because the investor was able to buy one of the best blue-chip stocks under $20.

Grindrod Shipping Holdings (GRIN)

Market Cap: $290 million

Grindrod Shipping Holdings (NASDAQ:GRIN) is a global dry bulk carrier based out of Singapore. The company is forecast to earn $6.63 this year, putting the stock on a forward multiple of just 2.4x.

In addition, the company pays a dividend of 47 cents per quarter or $1.88 per year. At $15.92 per share, that gives it a decent yield of 11.8% if the dividend is maintained at this level.

One reason the stock could be cheap is that it has a lot of debt. It has over $238 million in total debt, less $106.5 million in cash. That effectively means it pays a lot of interest. Last quarter’s interest expenses were $3 million per quarter or $12 million on an annual basis.

So far this year the stock up down 17%.

However, this provides an opportunity for value investors. For example, its tangible book value per share (TBVPS) now is $18.04 per share. At $15.92, the stock is trading for just 88.2% of TBVPS.

This also implies that if it were to rise to TBVPS, GRIN stock would have a 13.3% upside. Combined with its 2.4x P/E and its 11.8% dividend yield, this makes it a great value stock.

Genco Shipping and Trading Limited (GNK)

Market Cap: $689 million

Genco Shipping and Trading Ltd (NYSE:GNK) is another global dry bulk carrier shipping company based in the U.S. Its ships carry iron ore, coal, grains, steel products and other dry-bulk cargoes around the world.

Right now GNK stock is cheap at just 3.5x earnings. Moreover, its quarterly dividend just rose to 79 cents, or $3.16 annually if it stays at this level. That brings its annual yield to 18.6%.

The company has committed to reducing its debt levels, which are a drag on its income with interest expenses. This might be why this year the stock is up 6%.

GNK stock could be a good buying opportunity for investors, especially if the global recession does not come in as bad as forecasted.

For example, as of March 31, the company’s latest balance sheet shows that its TBVPS is $22.18 per share. That provides an opportunity for the stock to rise 30% over its present price if it were to rise to its TBVPS.

Cenovus Energy (CVE)

Market Cap: $31.29 billion

The next on our list of the best blue-chip stocks under $20, Cenovus Energy (NYSE:CVE), is a Canadian integrated oil and gas company based in Calgary. The company is very profitable and is forecast to produce earnings of $3.26 per share this year and $3.32 next year. That puts it on a cheap forward P/E multiple of just 5x for 2022 and 4.9x for 2023.

Moreover, the stock offers a dividend yield of 2% this year. Recently the company raised its dividend to 8.12 cents per quarter, putting it at an annual rate of 32.48 cents annually.

Moreover, the stock offers a good covered call income play opportunity. For example, the following chart shows that the Aug. 19 $20 calls are priced at 20 cents.

This means that the investor will receive $20 for every call contract. So for every 100 shares that cost $1,630, the investor gets to receive $20 for selling the $20 strike price calls that expire on Aug. 19.

This is a return of 1.23% for the month or 14.76% on an annual basis. And if the stock rises to $20 per share from $16.30, the investor keeps the 22.7% return. The total potential upside of 23.93% is a very good opportunity for most investors. This is especially since the stock costs less than $20 and the investor can sell many covered calls.

Ford Motor Company (F)

Market Cap: $45.79 billion

Ford Motor Co. (NYSE:F) stock is very cheap now, as earnings are forecast to rise 7.1% to $2.06 in 2023 from $1.92 in 2022. That puts the auto manufacturer that is trying to transition to the EV world (electric vehicles) at just 5.9x earnings for 2023 down from 6.3x in 2022.

Moreover, Ford stock pays a dividend of 40 cents per annum and, at $11.88 at Friday’s close, has a dividend yield of 3.4%. The company has been paying 10 cents now for the past three quarters after it resumed payments in late 2021.

Right now the Aug. 19 call options offer a good covered call opportunity, as the table below shows.

The $14 strike price calls about one month out are priced at 11 cents at the midpoint. On an annualized basis, that presents an annual yield of 11.1% to the patient investor, assuming it can be replicated each month.

Carlyle Secured Lending (CGBD)

Market Cap: $668 million

Carlyle Secured Lending (NYSE:CGBD) is a private equity business development company (BDC) that invests in the primary and secondary market for business loans. This includes purchasing bank loans made to middle-market companies.

As a result, the company passes on to its shareholders the vast majority of the interest earned. In fact, it has to pass on 90% of its net income. That is why CGBD stock now has a high dividend yield, over 10%.

Moreover, the stock trades on a reasonably low P/E multiple at 7.9x. This is the highest P/E of any stock on this list of the best blue-chip stocks to buy under $20.

Even more appealing is the fact that CGBD stock trades for just 74.4% of its tangible book value of $17.11. So, if the stock at $12.73 today rises to its TBVPS that will provide a 34.4% upside opportunity.

There is also a good opportunity to make money using this price target. The chart below shows that the $17.50 call options trade for 13 cents, or literally 1% over today’s price of $12.73 per share.

This means that the investor in CGBD calls one month out can make an annualized 12.24% return selling one-month-out covered calls. Assuming the stock does not rise by 34.4% over the month period that the calls are sold, the investor can also collect the 11.1% dividend yield.

So, this presents a unique opportunity to make up over 33% annually before any price moves on the stock (i.e., 11.1% dividend yield plus 12.2% covered call income).

On the date of publication, Mark Hake did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.